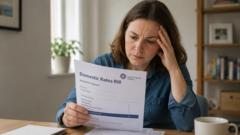

The annual arrival of the domestic rates bill is never a moment for celebration in Northern Ireland households. But lately, those paper envelopes are delivering a much sharper sting. As district rates climb across all eleven local councils, a quiet crisis is brewing right under the surface. More and more people simply can't pay.

While headline figures often focus on high-profile corporate bailouts or massive infrastructure deficits, the real economic strain is sitting on kitchen tables. Total uncollected rates debt across the region has previously hovered around staggering heights—reaching over £145 million in cumulative arrears carried forward by Land & Property Services (LPS). Millions of pounds are written off entirely every single year because the money simply cannot be recovered. If you enjoyed this piece, you might want to read: this related article.

If you think this is just a problem for the people who fall behind, you're mistaken. When a significant portion of the population defaults on their property taxes, the financial black hole impacts the bin collections, leisure centres, and regional roads that everyone relies on.

The Squeezed Middle and the Reality of Rates Arrears

Let's look at what's actually happening on the ground right now. The average household rate bill in Northern Ireland sits well over £1,200. With local authorities pushing through fresh hikes to keep up with their own inflationary pressures, families are finding themselves backed into a corner. For another look on this story, refer to the latest update from Associated Press.

A common misconception is that people who don't pay their rates are just trying to dodge their civic duties. The reality is far more clinical. The "squeezed middle"—households that earn too much to qualify for Universal Credit or specific rate reliefs, but too little to comfortably absorb consistent cost-of-living increases—is cracking.

When you're forced to choose between keeping the heating on, buying groceries, or paying a regional property tax, the tax bill usually gets shoved into a drawer. The trouble is, domestic rates aren't a casual subscription service you can just cancel. They are a priority debt.

What Happens When You Can't Pay

LPS doesn't wait around very long if you miss a payment. If you pay by monthly instalments and miss a date, the clock starts ticking immediately.

- The Seven-Day Warning: You get exactly seven days from the initial reminder to clear the missed instalment or set up an airtight alternative agreement.

- The Final Notice: If you ignore the warning, you lose the automatic right to pay in instalments. LPS will demand the full annual balance upfront within ten days.

- The Court Process: If the balance remains unpaid, LPS skips further reminders and takes you straight to the magistrate's court via a Process in Debt Proceedings. This adds instant legal costs to your original debt.

Once a decree is granted by the court, the enforcement mechanisms are severe. We aren't just talking about a bad mark on your credit file. The Enforcement of Judgments Office (EJO) can step in with aggressive recovery tactics. They can issue an Attachment of Earnings Order to pluck money directly from your monthly paycheck. They can place an Order Charging Land against your home, meaning the government gets its cut the moment your property is ever sold. If you owe more than £5,000, they can even initiate full bankruptcy proceedings.

The Structural Flaw in the System

The debate inside the Northern Ireland Assembly highlights a massive systemic frustration. Politicians regularly clash over the tens of millions of pounds written off by the Department of Finance. Critics rightly argue that it is deeply unfair to law-abiding households who scrape by to pay on time while massive sums slip through the cracks.

But the tools the government uses to fix the deficit often end up punishing the wrong people. For instance, recent policy debates have focused heavily on scaling back the early payment discount. Historically, ratepayers who paid their annual bill in full right away received a 4% discount. Proposals to slash that discount to 2% to claw back a projected £4 million in revenue feel like a slap in the face to households trying to do the right thing.

Taking away incentives from the people who actually pay doesn't solve the core issue of why others can't.

How to Protect Yourself If You're Struggling

If you're looking at a rate bill you can't afford, sitting on your hands is the absolute worst move. You need to treat this with the same urgency as a mortgage or rent payment.

First, check if you qualify for any existing safety nets. There's a 70% Lone Pensioner Discount if you're over 70 and live alone. There's a 25% Disabled Persons Allowance if your property has been physically adapted to meet specific medical needs. If you're on Universal Credit, don't assume your rates are automatically covered; you have to actively apply through the Rate Rebate Scheme.

Second, if you don't qualify for help but still can't make the math work, contact LPS before they contact you. Show up with a clear, realistic budget that outlines exactly what you have coming in and going out. If you can propose a sustainable payment plan to chip away at the arrears while covering your current bills, they are far more likely to work with you than if you wait until a court summons lands on your mat. Organizations like StepChange and Advice NI offer free, confidential guidance to help construct these budgets so you don't have to face the system alone.